Abstract

This study aims to determine the effect of Liquidity (Current Ratio), Solvency (Debt to Equity Ratio), and Activity (Total Assets Turnover) on profitability with measuring instruments (Return on Assets) in the cement sub-sector manufacturing industry in 2018- 2022. The data used in this study are annual financial report data on 6 cement companies listed on the Indonesia Stock Exchange for the period 2018-2022. The research method is quantitative with descriptive analysis. The classical assumption test performed includes multicollinearity test, autocorrelation test, and heteroscedasticity test. The results of the analysis use and hypothesis testing which includes determination analysis, partial test (t test), simultaneous test (F test) and uses multiple linear regression models. The results of this study indicate that, simultaneously Current Ratio, Debt to Equity Ratio, Total Assets Turnover affect Return on Assets sig value 0.000, with an Adjusted R-square value of 51.6%. Partially, Current Ratio has a positive but insignificant effect on ROA, Debt to Equity Ratio has a positive and significant effect on ROA, and Total Assets Turnover has a positive and significant effect on ROA.

Keywords

Current Ratio, Debt to Equity Ratio, Total Assets Turnover, Return on Assets

1. Introduction

Cement companies are industries that process raw materials into finished or semi- finished products with high value. The cement industry is one of the industries on the Indonesia Stock Exchange that attracts investor interest due to its role in Indonesia's growing infrastructure development. Cement is closely related to the real estate and property industry, as it is used in the construction of buildings.

Financial parameters such as Current Ratio (CR) and Return on Assets (ROA) can be used to assess the ability of cement companies to meet short-term obligations and earn profits. Examination of ROA data from six cement companies listed on the Indonesia Stock Exchange shows significant variation in ROA.

Financial parameters such as Current Ratio (CR) and Return on Assets (ROA) can be used to assess the ability of cement companies to meet short-term obligations and earn profits. An examination of the ROA data of six cement companies listed on the Indonesia Stock Exchange shows significant variation over the previous five years, which is indicative of the varying financial results of each company.

To evaluate the liquidity and profitability of a company, financial measures such as CR, DER, and TATO are essential. The company's ability to fulfil short-term obligations is measured by CR, the efficiency of using assets to generate revenue is measured by TATO, and the use of debt is measured by DER.

Eka Sutisna

DER has a negative effect on profitability (ROA) of -2.018. This can be interpreted as every one unit increase in the DER level, profitability will decrease by -2.018.

The purpose of this study

is to assess how the three ratios affect ROA in six cement companies listed on the IDX between 2018 and 2022, both simultaneously and partially. It aims to explain how internal and external variables affect the profitability of cement companies.

Research Objectives

1. to test how Return on Assets is affected by Current Ratio, Debt to Equity Ratio, and Total Asset Turnover.

2. To assess how Current Ratio affects Return On Asset..,

3. To see how return on assets is affected by the debt to equity ratio.

4. Determine the effect of Total Asset Turnover on Return on Assets.

2. Literature Review

Profitability

According to Harahap

| [3] | Harahap, S. S. (2015). Critical Analysis of Financial Statements (3rd ed.). Rajawali Press. |

[3]

financial ratios are numbers obtained by comparing elements of financial statements with other elements that have a relevant and significant (meaningful) relationship.

Liquidity

According to Riyanto

| [9] | Riyanto, B. (2012). Fundamentals of Management (Empa Edition). BPFE. |

[9]

alludes to the problem of the company's ability to meet its short-term financial obligations. The strength of a corporation is determined by the quantity of means of payment (liquid assets) it has at any one time.

Solvency

According to Harahap

| [4] | Harahap, S. S. (2016). Critical Analysis of Financial Statements. Rajawali press. |

[4]

defines solvency as the company's ability to meet its debts, both current and future, in the event of liquidation.

Activities

According to Hery

| [5] | Hery. (n. d.). Financial Statement Analysis. CAPS (Centre for Academic Publishing Service). |

[5]

is a ratio used to assess how well a business uses resources and other assets. This includes how efficiently a business uses its resources.

Previous Research

1. Sianipar

| [10] | Sianipar, B. (2016). The effect of liquidity, solvency, activity and profitability on firm value: Case study on PT Astra International Tbk. University of Indonesia. |

[10]

The effect of liquidity, solvency, activity, and profitability on business value at PT Astra Internasional Tbk listed on the Indonesia Stock Exchange is the subject of Sianipar's previous research. The purpose of this study was to determine simultaneously the ratio of activity, profitability, solvency, and liquidity to business value at PT Astra Internasional Tbk, a company listed on the Indonesia Stock Exchange. Based on the results of the study, liquidity, solvency, activity, and profitability of PT Astra Internasional Tbk have no significant effect on firm value, either wholly or partially. Therefore, it is very important for the business world to maintain its health condition so that investors remain interested in investing their money in the business.

2. Nuraisyah

| [7] | Nuraisyah, S. (2017). Analysis of the effect of liquidity, solvency and activity on profitability in the property and real estate sector listed on the Indonesian stock exchange for the period 2012-2013. Journal of Management and Accounting, 16, 1. |

[7]

Previous research conducted by Sasha Nuraisyah analysed the impact of liquidity, solubility and activity on profits in the real property and heritage segment listed on the IDX for the period 2012-2015. This study aims to determine the impact of liquidity (current proportion), solubility (obligation to increase the proportion of resources) and action (increase resource turnover) on productivity (return on resources) simultaneously. It asks about the strategy of labour inspection (purposeful testing). The type of research used is quantitative analysis using the E-Views 7 adaptation tool. The information preparation or investigation strategy used is the collection of supporting information by obtaining information and data indirectly sourced from the IDX and the company's official website by using the presumption testing instrument. classical which includes typical test, multicollinearity test, heteroscedasticity test, and autocorrelation test and speculation test using various direct relapse models which include assurance test, t test, and f test. The results show that (1) there is a simultaneous positive and important influence between liquidity (X1), solubility (X2), and movement (X3) on productivity (Y) of the property sector and genuine domain listed on the IDX, and (2) there is a partial negative and immaterial influence between liquidity (X1), solubility (X2) on benefits, while movement (X2) has a positive and significant half effect on benefits. From the investigation that has been conducted, it is concluded that the addition of resource turnover mostly has an impact on resource return. For a while, the other proportion has no impact on resource returns.

3. Muhammad

| [6] | Muhammad. (2016). Analysis of Return On Assets, Current Ratio, Debt to Equity Ratio, and Net Profit Mergin to Company Value (case study on manufacturing companies in the consumer goods sector listed on Bei for the 2011-2014 period. [University Islam NegriSyarif Hidayahtullah]. https://repostory.uinjkt.ac.id/35733/1pd |

[6]

Studies on the effect of return on assets, current ratio, debt to equity ratio, and net profit margin on firm value were conducted by Muhammad. This study involved manufacturing companies in the consumer goods industry sector listed on the IDX from 2011 to 2014. The purpose of this study was to analyse the variables variables that affect firm value in the financial statements filed on the Indonesia Stock Exchange. The research findings show that although current ratio has no effect on firm value, return on assets, debt-to-equity ratio, and profit margin have an effect.

4. Sharif

| [13] | Sharif. (2014). Analysis of the Effect of Financial Performance on Company Value (Case Study on Food And Beverage Companies Listed on the Indonesia Stock Exchange Year 2008-2012) [University Muhammadiyah]. https://eprints.ums.ac.id/30251 |

[13]

Research on "Analysis of financial performance on firm value (case study on food and beverage companies listed on the Indonesia Stock Exchange in 2008-2012)" was conducted by Syarif. This study looks at how financial performance such as current ratio (CR), debt to equity ratio (DER), and gross profit margin (GPM) affect the value of food and beverage companies listed on the Indonesia Stock Exchange in 2008 and 2012. The research findings show that debt-to-equity ratio, gross profit margin, and current ratio all affect firm value simultaneously. In contrast, DER partially has no effect, gross profit margin partially has an effect, and CR has no major effect on firm value.

5. Supardi, Suratno, and Suyatno

| [11] | Supardi, H., H. Suratno, H. S., & Suyanto, S. (2018). The Effect of Current Ratio, Debt To Asset Ratio, Total Asset Turnover and Inflation on Return on Asset. JIAFE (Scientific Journal of Accounting Faculty of Economics), 2(2), 16-27. https://doi.org/10.34204/jiafe.v2i2.541 |

[11]

Previously, research was conducted by Herman Supardi, H. Suratno and Suyatno, namely the Impact of Current Proportion, Proportion of Obligations to Resources, Increase in Resource Turnover and Expansion on Return On Resources. It aims to find out how much influence CR, DAR, TATO and expansion have on ROA in tamtama cooperatives in Agreeable Fund Services, Small and Medium Enterprises, Exchange and Industry in Indramayu Government in 2010-2014 so that it can be used as an administrative reference in decision making. It asks about work with a purposeful examination strategy, by utilising additional information. The information preparation or examination strategies utilised are various recurrence investigations. As a result of this, it can be seen that CR and swelling do not affect ROA, DAR and TATO have an impact on ROA, while CR, DAR, TATO and expansion affect ROA. It can be concluded that CR is too high due to the amount of resources or receivables that still exist.

6. Putra

| [8] | Putra, E. P. (2017). The Effect of Liquidity and Solvency on Profitability in Companies Listed on the Indonesia Stock Exchange (IDX) for the Period 2011-2015. Pakuan University. |

[8]

Research conducted by Putra specifically the Effect of Liquidity and Dissolvability on Profits in Companies Listed on the Indonesian Stock Exchange for the Period 2011-2015. It aims to determine how much impact liabilities, short-term liabilities, or long-term liabilities have on profits in broadcasting communication subsector companies listed on the Indonesia Stock Exchange (IDX). This kind of research is quantitative research with a test size of 5 years on the budget reports of broadcasting communication companies listed on the IDX for the 2011-2015 period. The preparation for information investigation that was carried out was firstly classical assumption testing and after that speculation testing was carried out. The measurable strategy used is various direct recurrences using SPSS. As for the results of this study, it was found that Liquidity (CR) and Dissolvability (DAR) together (together) have a positive and significant effect on the company's productivity (ROA), but most of the liquidity (CR) has a negative and immaterial impact, but the solvency (DAR) has a positive and important impact on productivity (ROA).

7. Alicia

| [1] | Alicia, D. D. (2017). The Effect of Liquidity and Solvency on Profitability in cement sub-sector companies listed on the Indonesia Stock Exchange. Pakuan University. |

[1]

Research conducted by Alicia, especially the Impact of Liquidity on Benefits in Cement Subsector Companies Listed on the Indonesia Stock Exchange for the Period 2011- 2015. This study aims to (1) determine the effect of current proportion on the proportion of return on resources in cement subsector companies listed on the Indonesia Stock Exchange for the period 2011-2015, (2) to determine the effect of fast proportion on the proportion of return on resources in cement subsector companies listed on the Indonesia Stock Exchange for the period 2011-2015, (3) to determine the effect of the proportion of money on the proportion of return on resources in cement subsector companies listed on the Indonesia Stock Exchange for the period 2011-2015, (4) to determine the effect of liquidity (current proportion, fast ratio, cash proportion) and the proportion of return on resources in cement subsector companies listed on the Indonesia Stock Exchange for the period 2011-2015. This type of research is quantitative in nature with the expository strategy used is an undoubted insight, using classical suspicion testing instruments and speculation testing and using various direct recurrence impressions. This investigation reveals that, presumably, the current proportion has a positive and critical impact on the proportion of return on resources and the proportion of money has no positive impact on the proportion of return on resources. Meanwhile, current proportion, quick proportion and cash proportion have a positive and critical impact on the proportion of return on resources.

8. Susanto, Heri and Kholis, N. (n.d.)

Research conducted by Heri Susanto and Nur Kholis is a study of the proportion of money related to the productivity of account management in Indonesia. It asks for points to analyse the impact of money-related proportion on productivity level with ROA intermediary, both partially and simultaneously. The creator used purposive examination method to gather public information from the financial statements of state-owned banks in 2007-2014. Information investigation utilised graphical insight, classical suspicion tests, various recurrence investigations, speculation testing and assurance coefficient (R2) examination. The results of this study indicate that the CAR, NPL and NIM factors have a significant influence on ROA, and the CR, LDER and BOPO factors have no influence on ROA, and the NIM variable has a dominant influence on ROA. Meanwhile, the synchronous factors of CAR, CR, NPL, NIM, LDR and BOPO have a considerable influence on ROA. Based on these results, the value is 81.1 per cent of the collateral coefficient R2.

Liquidity (CR) has a negative and insignificant effect on (ROA). This is indicated by the tcount CR value of -0.298 < ttable of 3. The statistical results of the t-test for the CR variable are 0.816 > 0.05. So it can be concluded that CR has a negative and insignificant effect on ROA. The negative effect indicates that there is a non-unidirectional relationship between CR and ROA. So this means that CR has a negative and insignificant effect. If there is an increase in CR, while other independent variables are considered constant, then this will not necessarily make ROA decrease, and vice versa, a decrease in CR does not necessarily cause ROA to increase.

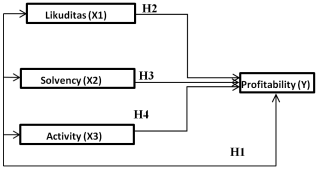

Thinking Framework

Figure 1. Research Paradigm.

3. Research Hypothesis

Hypotheses are presumptions or assumptions that must be proven through data or facts obtained through research. Based on the theoretical basis, previous research, conceptual framework, it can be concluded that several hypotheses in this study are as follows:

1. H1: Return on Assets is positively and significantly influenced by Current Ratio, Debt to Equity Ratio, and Total Assets Turnover simultaneously.

2. H2: Return on Assets is partially positively and significantly influenced by Current Ratio.

3. H3: Return on Assets is significantly and positively influenced by Debt to Equity Ratio.

4. H4: Return on assets is significantly and positively affected by partial turnover of total assets.

4. Research Methods

Type of Research

The quantitative data used in this study comes from the financial statements of cement subsector businesses listed on the IDX website for the period 2018-2022. The reports are accessed through the official websites of the relevant cement companies and http://www.idx.co.id.

Research Population and Sample

The study population is all changes in the cement subsector listed on the Indonesia Stock Exchange between 2018 and 2022. The following standards are used in sample selection:

1. Companies listed between 2018 and 2022 on the IDX.

2. Companies that issue complete audited financial statements.

3. Companies whose fiscal year ends on 31 December. Six companies were sampled based on these criteria

Data Collection Technique

Financial records of cement industry companies on the Indonesia Stock Exchange (IDX) website are used as the main secondary data source in this study. With a focus on audited annual reports for the period 2018-2022. This data collection is supported by literature studies from scientific journals, theses and books to strengthen the theoretical basis of the research.

Analysis Technique

The analysis technique that will be used in this research is multiple linear regression analysis.

5. Research Results

Table 1. Multicollinearity Test.

Model | Collinearity Statistics |

Tolerance | VIF |

1 (Constant) | | |

CR DER | .974 | 1.027 |

TATO | .980 | 1.020 |

.979 | 1.022 |

Dependent Variable: ROA

Source: Data processed by the author SPSS version 22

Table 1 above provides results that show that all independent variables have values greater than 0.1 and VIF values are less than 10. This indicates that multicollinearity problems are not detected by this regression model.

Table 2. Autocorrelation Test.Autocorrelation Test.Autocorrelation Test.

Model | R | R Square | Adjusted R Square | Std. Error of the Estimate | Durbin Watson |

1 | ,752a | ,566 | ,516 | 7503,56390 | 1,540 |

Predictors: (Constant), TATO, CR, DER

Dependet Variable: ROA

Source: Data processed by the author SPSS version 22

Based on the results of

table 2 above, it can be seen that the results of the Durbin Watson value obtained from the analysis results are 1.540. Because DW 1.540 which means in the normal range (0 < DW < 4), so it can be concluded that the regression model used does not occur autocorrelation in this regression model.

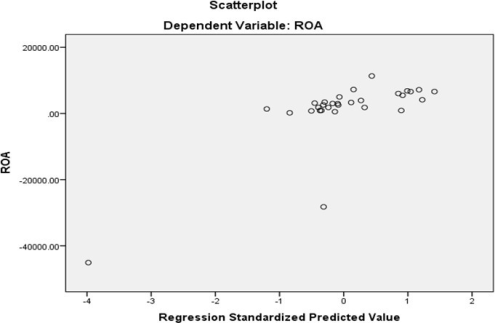

Heterocedacity Test

Figure 2. Heterocedasticity test.

It can be seen from

Figure 2 above that the distribution of points above and below the number 0 on the Y axis does not follow a visible pattern. This indicates that the study does not experience heteroscedasticity.

Multiple Linear Regression

Table 3. Multiple Linear Analysis.

Model | Unstandardised Coefficients | Standardised Coefficients | t | Sig. |

B | Std. Error | Beta |

1 (Constant) | -19868.924 | 5203,429 | | -3,818 | .001 |

CR | 3,415 | 1,818 | ,246 | 1,878 | .072 |

DER | -,027 | ,007 | -,464 | -3,553 | .001 |

TATO | 37,616 | 9,353 | ,525 | 4,022 | .000 |

Coefficientsa

a. Dependent Variable: ROA

Source: Data processed by the author SPSS version 22

From the table results, the regression equation is:

Y= -19868.924+3.145 X1-0.27 X2+37.616X3

The above equation for multiple linear regression models can be understood as follows:

1. Konstata

The constant value (a) of -19868.924. indicates if the value of all independent variables (X1, X2, and X3) is zero, then the value of Return on Assets (ROA) is expected to be -19868.924. This constant provides basic information about the value of ROA when the independent variables do not contribute.

2. The regression coefficient (b1) for current ratio is 3.415. This indicates that, assuming all other factors remain the same, an increase in the current ratio by one unit will result in an increase in return on assets of 3.415. This shows that Current Ratio and Return on Assets have a good relationship.

3. For the Debt to Equity Ratio variable (b2), the regression coefficient value is -0.027. This indicates that, if all other factors remain the same, an increase in the debt to equity ratio by one unit will result in a decrease in return on assets of 0.027. The fact that there is a negative correlation indicates that an increase in the debt-to-equity ratio can reduce return on assets.

4. For the Total Assets Turnover variable (b3), the regression coefficient value is 37.616. This indicates that, assuming all other factors remain the same, a one-unit increase in total assets turnover will result in an increase in return on assets of 37.616. Return on Assets and Total Assets Turnover have a strong positive correlation.

Determination Test R2

Table 4. Determination Test R2.

Model | R | R Square | Adjusted R Square | Std. Error of the Estimate |

1 | ,752a | ,566 | ,516 | 7503.56390 |

Model Summary

a. Predictors: (Constant), TATO, DER, CR Source: Data processed by the author of SPSS version 22

The analysis findings show that 51.6% or 0.516 is the Adjusted R Square. This shows that Current Ratio, Debt to Equity Ratio, and Total Assets Turnover contribute about 51.6% to fluctuations in the Return on Assets ratio, and the remaining 48.4% is influenced by other factors.

Determination Test R2

Table 5. The t- test.

Model | Unstandardised Coefficients | Standardised Coefficients | t | Sig |

B | Std. Error | Beta |

1 (Constant) | -19868.924 | 5203.429 | | -3.818 | .001 |

CR | 3.415 | 1.818 | .246 | 1.878 | .072 |

DER | -.027 | .007 | -.464 | -3.553 | .001 |

TATO | 37.616 | 9.353 | .525 | 4.022 | .000 |

Coefficientsa

a. Dependent Variable: ROA

Source: Data processed by the author SPSS version 22

1. Liquidity (Current Ratio) to Profitability (Return on Assets)

Profitability Ratio (Return on Assets) to Liquidity (Current Ratio). Return on Assets is significantly positively affected by Current Ratio. The tcount value of Current Ratio of 1.878> ttabel of 1.708 illustrates this. For the Current Ratio variable, the t test statistical finding is 0.072 <0.05. Thus, it can be said that Return on Assets is significantly positively influenced by Current Ratio. The positive effect illustrates the unidirectional relationship between CR and ROA. Then it means H2 is accepted H0 is rejected.

2. Solvency (Debt to Equity Ratio) to Profitability (Return on Assets)

Return on Assets is significantly and negatively affected by Debt to Equity Ratio. This can be seen from the calculated Debt to Equity Ratio of -3.553> ttabel of 1.708. The statistical test results for the Debt to Equity Ratio variable show 0.001> 0.05. Thus, it can be said that Return on Assets is significantly influenced by Debt to Equity Ratio. The unidirectional relationship between Debt to Equity Ratio and Return on Assets is indicated by a negative effect. This shows that H0 is approved and H3 is not.

3. Activity (Total Assets Turnover) to Profitability (Return on Assets)

Return on Assets benefits greatly from Total Assets Turnover. Thitung of 4.022

> ttabel of 1.708 indicates this. For the Total Assets Turnover variable, the t-test statistical finding is 0.000 > 0.05. Thus, it can be said that Return on Assets is positively and significantly influenced by Total Assets Turnover. The positive effect shows the relationship between TATO and ROA. This indicates that H0 is rejected and H4 is accepted.

F test

Table 6. F-test.

Model | Sum of Squares | df | Mean Square | F | Sig. |

1 Regression | ,817 | 3 | ,939 | 11.292 | ,000b |

Residuals | ,650 | 26 | ,256 | | |

Total | ,467 | 29 | | | |

ANOVAa

a. Dependent variable: ROA

Predictors: (Constant), TATO, DER, CR

Data source: Data processed by the author SPSS version 22

Table 6 shows that the F count is 11.292 with a significance of 0.00. It can be seen that the significance value is greater than 0.05. It can be concluded that the variables of Liquidity

(Current Ratio), Solvency

(Debt to Equity Ratio), and Activity

(Total Assets Turnover) together have no significant effect on Profitability

(Return on Assets). 6. Discussion

Relationship between Current Ratio and Return on Assets

Based on incomplete research findings, Return on Assets which is the dependent variable (Y) is not affected by Current Ratio which is the independent variable (X1). This problem indicates that the company has enough current assets to pay its short-term liabilities. But there is a negative impact to consider. The higher the Current Ratio, the more likely the company has invested too much current assets. This means the company loses the opportunity to generate higher profits by allocating those funds to more profitable investments.

This study shows that the results of the study are not in line with the initial hypothesis which assumes that Current Ratio has a positive and significant effect on Return on Assets. However, from the results of this study, the Current Ratio has a positive but insignificant effect.

But this research is in line with previous research conducted by Putra which states that Current Ratio (simultaneously) has a positive and significant effect on the company's Return on Assets, but partially Current Ratio has a negative and insignificant effect on Return on Assets.

Relationship between Debt to Equity Ratio and Return on Assets (ROA)

Partial research findings show that Return on Assets (ROA) which is the dependent variable (Y) is significantly influenced by Debt to Equity Ratio (DER) which is the independent variable (X2). This shows that interest rates increase along with the percentage of debt in a company's capital structure. The research hypothesis is supported by this study.

This study supports previous research conducted by Syarif which found that debt to equity ratio and current ratio both affect firm value simultaneously.

Relationship between Total Assets Turnover and Return on Assets (ROA)

Partial results show that Return on Assets (ROA) which is the dependent variable (Y) has a significant positive effect on Total Assets Turnover which is the independent variable (X3). This shows that for a business to be profitable, high sales must occur after the use of assets to create total net sales. The idea is supported by this research.

This study supports previous research conducted by Supardi et al. which found that in addition to TATO affecting ROA, inflation also has an impact on ROA.

Relationship between Current Ratio (CR), Debt to Equity Ratio (DER) and Total Assets Turnover (TATO) with Return on Assets (ROA)

Debt to Equity Ratio, Total Assets Turnover, and Current Ratio all increase Return on Assets significantly when used collectively, according to research conducted simultaneously. This shows that in a company that plays a significant role in boosting profitability, the influence of Current Ratio, Debt to Equity Ratio, and Total Assets Turnover has a value that plays an important role in increasing Return on Assets. The research hypothesis is supported by this study.

This study supports previous research conducted by Shasha Nuraisyah which found that Return on Assets (ROA) is positively and significantly influenced by Current Ratio (CR), Debt to Equity Ratio (DER), and Total Assets Turnover (TATO).

7. Conclusions and Suggestions

7.1. Conclusion

The effect of activity, solvency, and liquidity on profitability in the cement subsector manufacturing industry has been investigated in this study. Based on the explanation that has been given previously, researchers can make the following reduction:

Debt to Equity Ratio, Current Ratio, and Total Assets Turnover have a large influence on cement subsector companies and return on assets. These results indicate that liquidity structure, capital structure, and asset utilisation efficiency have a significant role in determining the company's return on assets.

In cement subsector companies, the Current Ratio variable has a positive but insignificant effect on Return on Assets. This shows that it will benefit the business to fulfil its direct responsibilities.

In cement subsector companies, Return on Assets is significantly and partially positively affected by the Debt to Equity Ratio variable. This shows that a company's income decreases as the level of debt in its capital structure increases and interest rates increase.

In cement sub-sector companies, Return on Assets is positively and somewhat significantly influenced by the Total Assets Turnover variable. This shows that Fast asset turnover combined with strong sales can generate profits when assets are utilised to create net sales.

7.2. Suggestions

Based on the research findings and conclusions previously described, the author seeks to propose several recommendations, specifically as follows:

Companies are advised to consider the capital structure in their financial strategy. This study suggests that companies should improve the efficiency of debt usage to maximise profitability without ignoring financial risks. In addition, the company should conduct regular evaluations of the capital structure and investment strategy to ensure that the level of debt used supports the improvement of overall financial performance.

For the company, it is recommended that the company focus on increasing the efficiency of asset use to increase profitability. The company needs to evaluate and optimise operational processes in order to maximise the results of each unit of assets owned. Investment in technology and better management can help improve productivity and efficiency. Further research can explore the factors that affect TATO and its impact in other industrial sectors to broaden the understanding of how to improve ROA.

For future researchers, it is recommended to investigate the mechanism of the relationship between DER, TATO, and ROA. Research could focus on how changes in DER and TATO affect ROA directly or indirectly. For example, analyses could explore whether an increase in DER leads to an increase in interest costs which reduces ROA, or how efficient use of assets (TATO) contributes to higher profits.

Abbreviations

CR | Curent Ratio |

DER | Debt to Equity Ratio |

IDX | Indonesia Stock Exchange |

ROA | Return on Asset |

TATO | Total Asset Turnover |

Author Contributions

Eka Sutisna is the sole author. The author read and approved the final manuscript.

Conflicts of Interest

The author states that there is no conflict of interest.

References

| [1] |

Alicia, D. D. (2017). The Effect of Liquidity and Solvency on Profitability in cement sub-sector companies listed on the Indonesia Stock Exchange. Pakuan University.

|

| [2] |

Eka Sutisna (2022) The Effect of Liquidity, Activity, and Solvency on Profitability in PT. Indofood Sukses Makmur Tbk nternational Journal of Social Science And Human Research

https://jurnalfebi.iainkediri.ac.id/index.php/proceedings

|

| [3] |

Harahap, S. S. (2015). Critical Analysis of Financial Statements (3rd ed.). Rajawali Press.

|

| [4] |

Harahap, S. S. (2016). Critical Analysis of Financial Statements. Rajawali press.

|

| [5] |

Hery. (n. d.). Financial Statement Analysis. CAPS (Centre for Academic Publishing Service).

|

| [6] |

Muhammad. (2016). Analysis of Return On Assets, Current Ratio, Debt to Equity Ratio, and Net Profit Mergin to Company Value (case study on manufacturing companies in the consumer goods sector listed on Bei for the 2011-2014 period. [University Islam NegriSyarif Hidayahtullah].

https://repostory.uinjkt.ac.id/35733/1pd

|

| [7] |

Nuraisyah, S. (2017). Analysis of the effect of liquidity, solvency and activity on profitability in the property and real estate sector listed on the Indonesian stock exchange for the period 2012-2013. Journal of Management and Accounting, 16, 1.

|

| [8] |

Putra, E. P. (2017). The Effect of Liquidity and Solvency on Profitability in Companies Listed on the Indonesia Stock Exchange (IDX) for the Period 2011-2015. Pakuan University.

|

| [9] |

Riyanto, B. (2012). Fundamentals of Management (Empa Edition). BPFE.

|

| [10] |

Sianipar, B. (2016). The effect of liquidity, solvency, activity and profitability on firm value: Case study on PT Astra International Tbk. University of Indonesia.

|

| [11] |

Supardi, H., H. Suratno, H. S., & Suyanto, S. (2018). The Effect of Current Ratio, Debt To Asset Ratio, Total Asset Turnover and Inflation on Return on Asset. JIAFE (Scientific Journal of Accounting Faculty of Economics), 2(2), 16-27.

https://doi.org/10.34204/jiafe.v2i2.541

|

| [12] |

Susanto, Heri and Kholis, N. (n.d.). Analysis of Financial Ratios on Profitability in Indonesian Banking. E-Journal LP3M STIEBANK, 7 (ISSN), 2442-4439.

http://www.ebbank.stiebbank.ac.id/index.php/EBBANK/article/view/83

|

| [13] |

Sharif. (2014). Analysis of the Effect of Financial Performance on Company Value (Case Study on Food And Beverage Companies Listed on the Indonesia Stock Exchange Year 2008-2012) [University Muhammadiyah].

https://eprints.ums.ac.id/30251

|

Cite This Article

-

APA Style

Sutisna, E. (2024). The Influence of Liquidity, Solvency, Activity on Profitability in the Cement Sub-Sector Manufacturing Industry Listed on the Indonesian Stock Exchange (Bei) for the Period 2018-2022. International Journal of Economics, Finance and Management Sciences, 12(6), 363-371. https://doi.org/10.11648/j.ijefm.20241206.12

Copy

|

Copy

|

Download

Download

ACS Style

Sutisna, E. The Influence of Liquidity, Solvency, Activity on Profitability in the Cement Sub-Sector Manufacturing Industry Listed on the Indonesian Stock Exchange (Bei) for the Period 2018-2022. Int. J. Econ. Finance Manag. Sci. 2024, 12(6), 363-371. doi: 10.11648/j.ijefm.20241206.12

Copy

|

Download

AMA Style

Sutisna E. The Influence of Liquidity, Solvency, Activity on Profitability in the Cement Sub-Sector Manufacturing Industry Listed on the Indonesian Stock Exchange (Bei) for the Period 2018-2022. Int J Econ Finance Manag Sci. 2024;12(6):363-371. doi: 10.11648/j.ijefm.20241206.12

Copy

|

Download

-

@article{10.11648/j.ijefm.20241206.12,

author = {Eka Sutisna},

title = {The Influence of Liquidity, Solvency, Activity on Profitability in the Cement Sub-Sector Manufacturing Industry Listed on the Indonesian Stock Exchange (Bei) for the Period 2018-2022

},

journal = {International Journal of Economics, Finance and Management Sciences},

volume = {12},

number = {6},

pages = {363-371},

doi = {10.11648/j.ijefm.20241206.12},

url = {https://doi.org/10.11648/j.ijefm.20241206.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijefm.20241206.12},

abstract = {This study aims to determine the effect of Liquidity (Current Ratio), Solvency (Debt to Equity Ratio), and Activity (Total Assets Turnover) on profitability with measuring instruments (Return on Assets) in the cement sub-sector manufacturing industry in 2018- 2022. The data used in this study are annual financial report data on 6 cement companies listed on the Indonesia Stock Exchange for the period 2018-2022. The research method is quantitative with descriptive analysis. The classical assumption test performed includes multicollinearity test, autocorrelation test, and heteroscedasticity test. The results of the analysis use and hypothesis testing which includes determination analysis, partial test (t test), simultaneous test (F test) and uses multiple linear regression models. The results of this study indicate that, simultaneously Current Ratio, Debt to Equity Ratio, Total Assets Turnover affect Return on Assets sig value 0.000, with an Adjusted R-square value of 51.6%. Partially, Current Ratio has a positive but insignificant effect on ROA, Debt to Equity Ratio has a positive and significant effect on ROA, and Total Assets Turnover has a positive and significant effect on ROA.

},

year = {2024}

}

Copy

|

Download

-

TY - JOUR

T1 - The Influence of Liquidity, Solvency, Activity on Profitability in the Cement Sub-Sector Manufacturing Industry Listed on the Indonesian Stock Exchange (Bei) for the Period 2018-2022

AU - Eka Sutisna

Y1 - 2024/11/21

PY - 2024

N1 - https://doi.org/10.11648/j.ijefm.20241206.12

DO - 10.11648/j.ijefm.20241206.12

T2 - International Journal of Economics, Finance and Management Sciences

JF - International Journal of Economics, Finance and Management Sciences

JO - International Journal of Economics, Finance and Management Sciences

SP - 363

EP - 371

PB - Science Publishing Group

SN - 2326-9561

UR - https://doi.org/10.11648/j.ijefm.20241206.12

AB - This study aims to determine the effect of Liquidity (Current Ratio), Solvency (Debt to Equity Ratio), and Activity (Total Assets Turnover) on profitability with measuring instruments (Return on Assets) in the cement sub-sector manufacturing industry in 2018- 2022. The data used in this study are annual financial report data on 6 cement companies listed on the Indonesia Stock Exchange for the period 2018-2022. The research method is quantitative with descriptive analysis. The classical assumption test performed includes multicollinearity test, autocorrelation test, and heteroscedasticity test. The results of the analysis use and hypothesis testing which includes determination analysis, partial test (t test), simultaneous test (F test) and uses multiple linear regression models. The results of this study indicate that, simultaneously Current Ratio, Debt to Equity Ratio, Total Assets Turnover affect Return on Assets sig value 0.000, with an Adjusted R-square value of 51.6%. Partially, Current Ratio has a positive but insignificant effect on ROA, Debt to Equity Ratio has a positive and significant effect on ROA, and Total Assets Turnover has a positive and significant effect on ROA.

VL - 12

IS - 6

ER -

Copy

|

Download